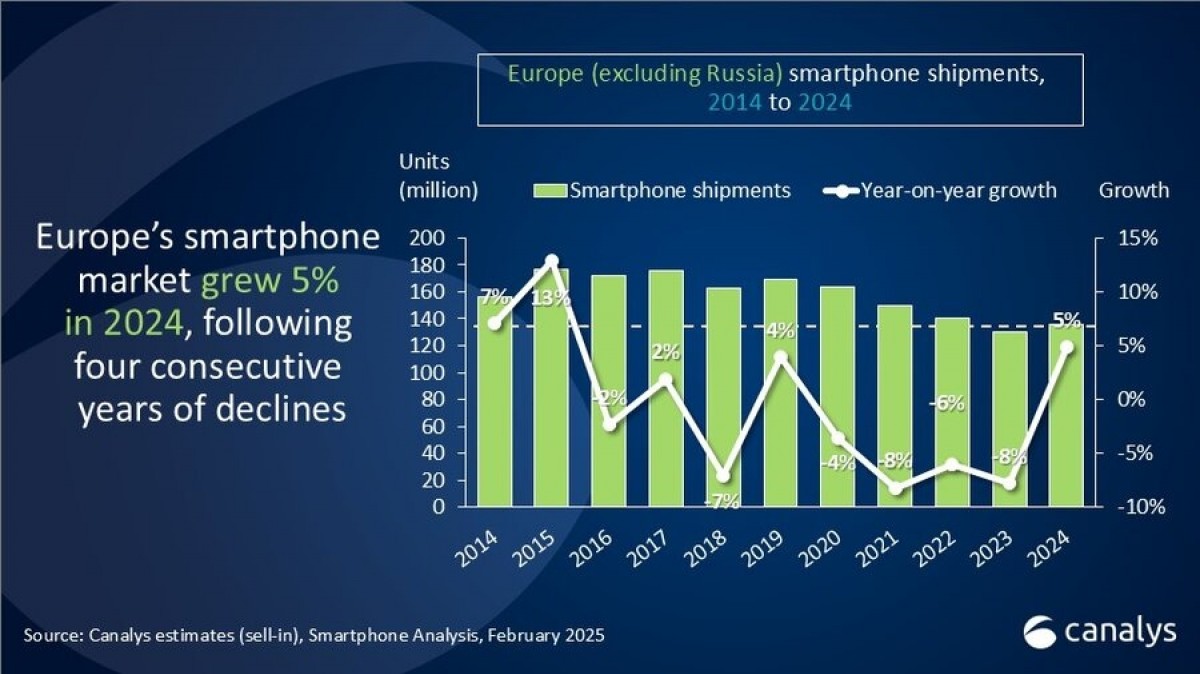

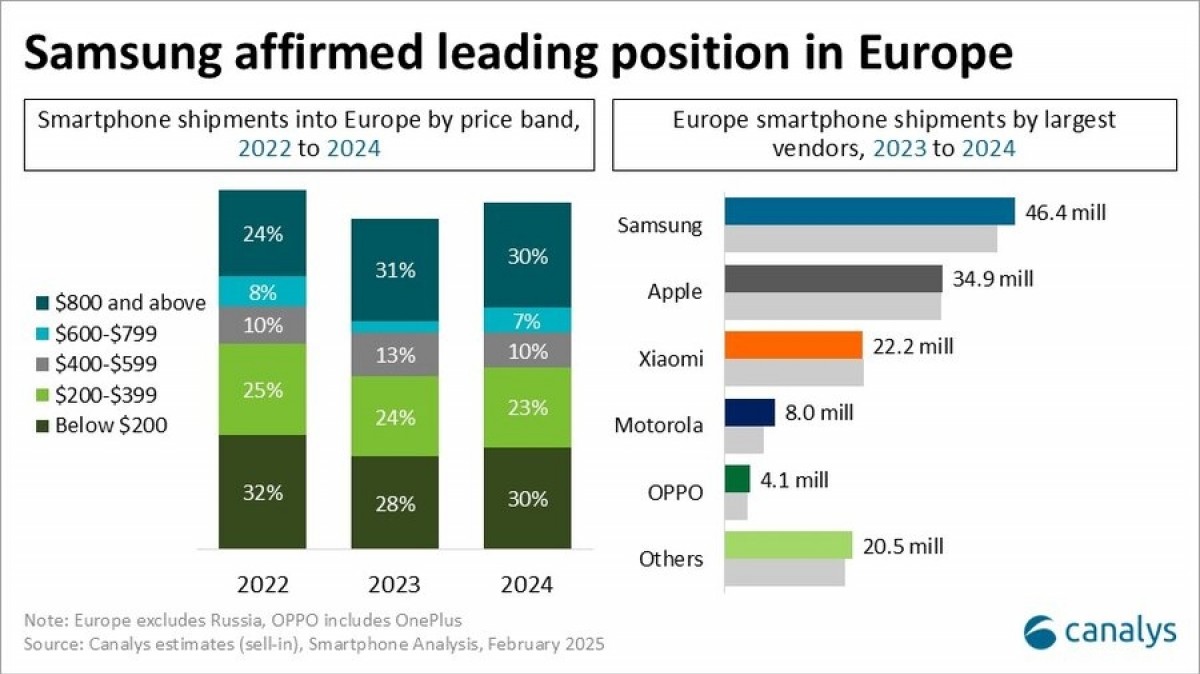

The smartphone market in Europe grew by 5% in 2024, following four consecutive years of decline. The announcement came from Canalys, which revealed the market saw just over 136 million devices shipped, with 30% of them being premium devices, priced $800 and above.

Samsung remained a leader in 2024, but Apple recorded impressive Q4 2024 sales. This was driven by a positive reception for the iPhone 16, even though ot still lacks Apple Intelligence.

The market saw resilient high-end demand, combined with a replacement cycle of mid-to-low-end smartphones, purchased during the pandemic. Samsung increased its sales by 6% on a yearly basis, while Apple shipped 1% more iPhones.

Xiaomi, the third biggest smartphone vendor in Europe, basically pushed the same amount of Redmi, Poco, and Xiaomi-branded phones as it did in 2023. Motorola saw a 26% increase, while Oppo grew 13% YoY, but Canalys pointed out the number includes OnePlus shipments.

The report points out that 2024 saw the biggest amount of premium devices sold – 41 million, or 30% of the total 136 million. The analysis is based on shipments and not actual store sales, and it includes Apple’s push of iPhone 13 and iPhone 14 devices into the channel before they were discontinued due to the USB-C directive; retailers are allowed to sell these devices if they were already on the shelves before December 28, when the directive kicked in.

Samsung’s increase in sales was mostly driven by the Galaxy S24 series, which was heavily advertised during the Paris 2024 Olympics.

A detailed analysis into separate countries revealed that Apple has almost double the Samsung shipments in the UK (52% vs 28%), but in Spain, it fell to third place, as Xiaomi shipped more phones than its Korean competitor

Motorola reached an all-time high in Europe in 2024, thanks to expansion through offline stores and open market channels. Oppo’s volume returned to growth after two difficult years, seeing a push in Southern Europe – Spain, Italy, Romania, and Portugal. Honor and Realme also grew by double digits, “intensifying competition and creating excitement within the channel and among consumers.”

| 2024 shipments (in million) |

2024 market share |

2023 shipments (in million) |

2023 market share |

Annual growth | |

| Samsung | 46.4 | 34% | 43.7 | 34% | 6% |

| Apple | 34.9 | 26% | 34.6 | 27% | 1% |

| Xiaomi | 22.2 | 16% | 22.2 | 17% | 0% |

| Motorola | 8.0 | 6% | 6.4 | 5% | 26% |

| Oppo | 4.1 | 3% | 3.7 | 3% | 13% |

| Others | 20.5 | 15% | 19.2 | 14% | 7% |

| Total | 136.1 | 100% | 129.8 | 100% | 5% |

Companies are facing a “complex 2025” as the EU will introduce an Ecodesign Directive on June 20, pushing manufacturers of mobile devices to prioritize longevity, ease of repair, and responsible resource use. This includes providing spare parts for several years, maintaining longer software support, and offering technical documentation to facilitate repairs by third-party providers.

Shortly put, vendors must launch phones with easily replaceable batteries and multiple years of software support. This is a huge challenge for most companies, and we are about to see them realign their priorities and target revenue growth from services, B2B plans and channel expansions.

Source link